| NEWS AND ANALYSIS |

|

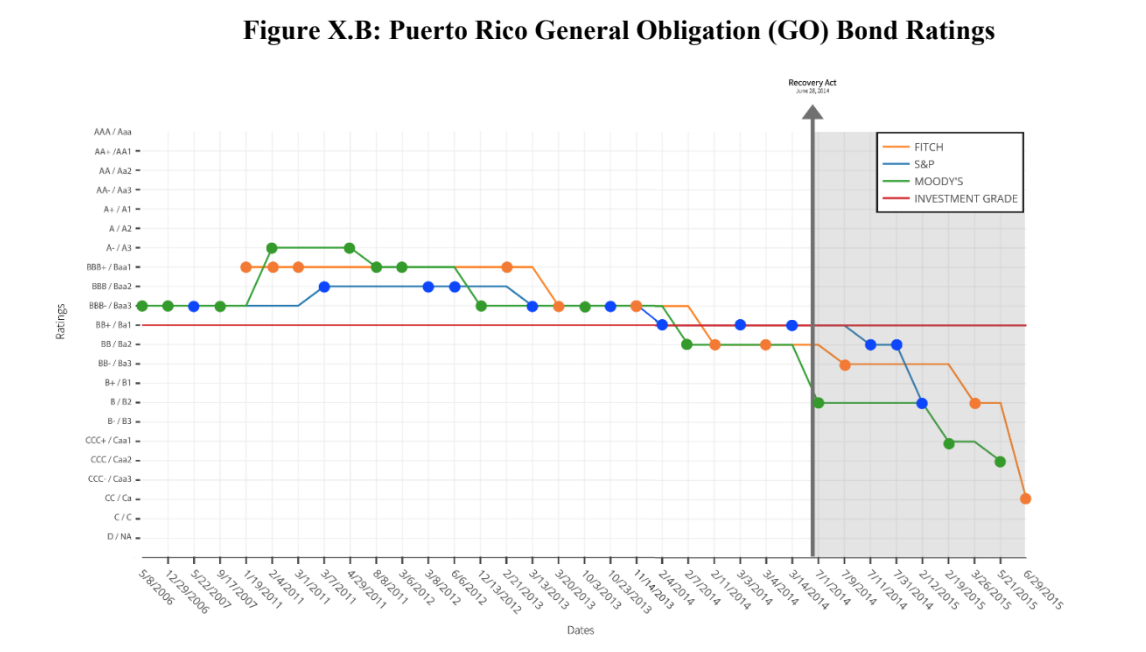

Commentary: Puerto Rico’s Biggest Bond Challenge Is Yet to Come*

Puerto Rico yesterday took a significant step in announcing a deal with its sales-tax bondholders, but the most-scrutinized deal for the commonwealth — and the $3.8 trillion municipal market as a whole — is still to come, according to a Bloomberg News commentary. According to Governor Ricardo Rossello, the deal on Cofina bonds would save the commonwealth $17.5 billion in interest payments over the life of the securities. While that sounds like a victory, bondholders come out quite nicely, too. Owners of senior Cofinas, with the highest claim on sales taxes, would recoup 93 percent of their investment, while subordinated securities get a 56 percent recovery. However, the fate of Puerto Rico’s roughly $18 billion general-obligation bonds, backed by the island’s full faith and credit, remains firmly in limbo. In theory, because Cofina securities will now have the first right to 53.65 percent of collected sales taxes, that should free up cash for G.O. debt. Court documents filed in June essentially said as much, adding that the extra funds could also cover essential services. It’s telling, though, that Puerto Rico’s benchmark general-obligation bond is still trading at 50 cents. On the one hand, that’s the highest price since Hurricane Maria devastated the island more than 10 months ago. But for debt that’s perceived to have at least equal standing to senior Cofinas, it has an awfully long way to go to catch up to the announced recovery rate, according to the commentary.

*The views expressed in this commentary are from the author/publication cited, are meant for informative purposes only, and are not an official position of ABI.

|

|

Analysis: U.S. Supreme Court to Decide Whether FDCPA Applies to Non-Judicial Foreclosures

Currently, some courts allow borrowers to bring Fair Debt Collection Practices Act claims for non-judicial foreclosures, while other courts do not, but that is about to change, according to an analysis in the Lexology blog. On June 28, the Supreme Court agreed to hear the appeal of Dennis Obduskey, a Colorado borrower arguing that the FDCPA should apply to non-judicial foreclosures. In the Tenth Circuit’s decision, a borrower sued his mortgage servicer and McCarthy & Holthus LLP, the law firm hired to process the non-judicial foreclosure, for failing to comply with certain requirements of the FDCPA. Specifically, Obduskey alleged that the law firm failed to respond to his request for a validation of the debt. The Tenth Circuit held that Wells Fargo was not a debt collector under the FDCPA, since it began servicing the loan before it went into default. That holding will stand and will not be heard by the Supreme Court. Significantly, the Tenth Circuit further held that the law firm was not a debt collector under the FDCPA because non-judicial foreclosure proceedings are not covered by the FDCPA. In doing so, the Tenth Circuit sided with the Ninth Circuit, holding that compliance with the FDCPA is not required during non-judicial foreclosure proceedings, contrary to the position of the Fourth, Fifth and Sixth Circuits. This is the holding that the Supreme Court will consider.

|

|

Commentary: Kavanaugh on the Executive Branch: PHH Corp. v. Consumer Financial Protection Bureau*

Judge Brett Kavanaugh, President Trump's nominee to the Supreme Court, wrote two opinions in PHH Corp. v. Consumer Financial Protection Bureau: a panel opinion declaring an aspect of the bureau to be unconstitutional, and an opinion dissenting from the en banc U.S. Court of Appeals for the District of Columbia Circuit’s decision overruling his panel opinion, according to a blog post on SCOTUSBlog. In both opinions, Kavanaugh expressed serious skepticism of the regulatory state while celebrating a view of the Constitution that vests in the president an extensive degree of unilateral authority over the executive branch’s enforcement of federal laws. Those views have been lauded by conservative commenters who celebrate Kavanaugh’s “[t]aming” of “the administrative state” — and by the White House, which has praised his record of “protect[ing] American businesses from illegal job-killing regulation.” Commenters on the left see in Kavanaugh’s PHH opinions a hostility to the CFPB’s mission more than to its structure, detecting an anti-consumer bias and general hostility to financial regulation.

*The views expressed in this commentary are from the author/publication cited, are meant for informative purposes only, and are not an official position of ABI.

How has the SCOTUS confirmation hearing process in the Senate changed from previous nominations? What comes next for Judge Brett Kavanaugh? Watch ABI Editor-at-Large Bill Rochelle discuss the process with ABI's Sam Gerdano, former chief counsel to Senate Judiciary Committee Chair Charles Grassley (R-Iowa). Click here.

|

|

U.S. Seafood Industry Vulnerable to Tariffs Aimed at China

The next round of U.S. tariffs aimed at Chinese imports could wind up hurting a major product that initially comes from America: fish, the Wall Street Journal reported. Proposed 10 percent duties by the Trump administration last month on $200 billion worth of imports from China included dozens of varieties of fish, from tilapia to tuna. The proposed tariffs, which could increase to 25 percent, are set to be decided in September by trade representatives. An estimated $900 million worth of fish and seafood on that list is first caught in the U.S., sent to China for processing into items like fish sticks and fillets, then imported by U.S. companies to sell to American consumers. The practice of sending fish to China to be breaded, seasoned, portioned or packaged has grown in the past two decades, according to U.S. fishing groups. Domestic seafood-processing plants have faced high costs and labor shortages, while cheaper facilities have sprung up in China to support its extensive domestic fish-farming industry. That has helped make China the top source of seafood to the U.S., with the 1.3 billion pounds sent to the U.S. last year double that of second-ranked India, according to market-research firm Urner Barry.

|

|

Trump Administration Cuts Staff at Financial Markets Watchdog

The Trump administration moved yesterday to shrink a government agency tasked with identifying looming financial risks, notifying around 40 staff members that they would be laid off, Reuters reported. The employees at the Office of Financial Research (OFR) were formally told yesterday that they will lose their jobs as part of a broader reorganization of the agency that was created in the wake of the 2007-09 global financial crisis. Staff at the OFR, an independent bureau within the U.S. Treasury that analyzes market trends to spot financial risks, were told in January that jobs would be eliminated as the administration sought to cut the OFR’s budget by 25 percent to around $76 million.

|

|

States Spar with Trump Administration over Fintech Oversight

The Trump administration’s plan to expand the federal government’s role in overseeing financial-technology startups has prompted pushback from some states, setting up a fight over who will regulate new markets for online lending and other banking products, the Wall Street Journal reported. “What I’d like to see is for the federal government to step back or enter cooperative agreements with states,” said Mark Brnovich, Arizona’s Republican attorney general. Arizona recently launched its own “sandbox” initiative meant to encourage companies to work with state officials to test new financial products and business models. Now, it and other states that are courting fintech companies with state licenses and rules have another competitor in the federal government. The U.S. Treasury Department last week released a report calling on financial regulators to embrace fintech developments, and the Office of the Comptroller of the Currency said that it would accept applications for banking charters from startups. The Consumer Financial Protection Bureau and Commodity Futures Trading Commission in recent weeks and months have both launched their own sandbox initiatives. State officials fear the federal push will limit their states’ ability to influence new businesses to the benefit of consumers in their states. One worry is that federal financial agencies will override state usury laws against excessive interest rates.

|

|

Notice to All ABI Members

UNITE HERE Local 11 is a labor union based in southern California. They represent more than 20,000 workers in the hotel and restaurant industry. The union has been attempting to organize employees at the Terranea Resort, site of ABI’s 2019 Winter Leadership Conference (WLC). UNITE HERE Local 11 is known for their aggressive tactics, both on site and also aimed at hotel clients. The union has repeatedly contacted ABI leadership, including members of the board and committee leaders, to urge ABI to cancel or move the WLC. ABI has no plans to move or cancel the event, which would result in substantial legal exposure. If you are contacted by phone or email by representatives of the union, ABI encourages you to ignore rather than engage or respond. ABI regrets this development and will continue to closely follow events at the property.

|

|

Sign up Today to Receive Rochelle’s Daily Wire by E-mail!

Have you signed up for Rochelle’s Daily Wire in the ABI Newsroom? Receive Bill Rochelle’s exclusive perspectives and analyses of important case decisions via e-mail!

Tap into Rochelle’s Daily Wire via the ABI Newsroom and Twitter!

|

|

| |

| BLOG EXCHANGE |

|

New on ABI's Bankruptcy Blog Exchange: House Panel Plans FHFA Oversight Hearing

The House Financial Services Committee has scheduled an FHFA oversight hearing for September in the wake of waste, fraud and abuse allegations, according to a recent blog post.

To read more on this blog and all others on the ABI Blog Exchange, please click here.

|

|

|

|